This added layer of transparency aims to give investors and stakeholders a clearer understanding of a company’s financial health and decision-making processes. Dollar-Value LIFO operates on the principle of valuing inventory in terms of dollars rather than physical units. This method aggregates inventory into pools based on their dollar value, which helps in simplifying the tracking of inventory layers.

It allows companies to match current costs with current revenues, providing a more accurate reflection of profitability. The pools created under this method are, therefore, known as dollar-value LIFO pools. Under the regular LIFO method, inventory is measured in units and is priced at unit prices. Under the dollar value LIFO method, inventory is measured in dollars and is adjusted for changing price levels.

There is software that can automate these calculations and provide real-time inventory updates, making life much easier. Choose a suitable price index that truly reflects your inventory’s price change. You could even consider indices such as Consumer Price Index a cost which changes in proportion to changes in volume of activity is called (CPI) or Producer Price Index (PPI), depending on your business nature. The two primary components of a Dollar Value LIFO inventory are the inventory pool and the price index. The base year is the year from which the Dollar Value LIFO calculations start.

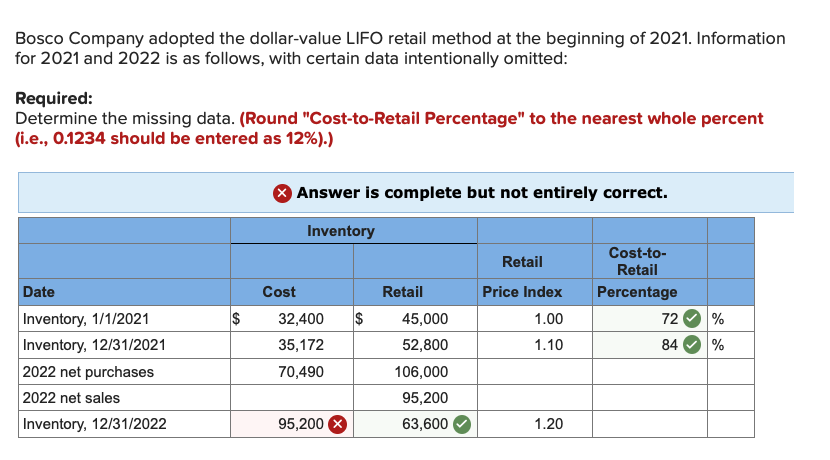

One thing worth mentioning again is that dollar-value LIFO pools the inventory up. In simple words we will have one total figure of all the different types of inventory we like to have in one pool. Dollar-value LIFO is a modification of traditional LIFO method in which ending inventory is measured on the basis of monetary value of units instead of quantity of units held. The base year is 2021, and you have 100 units in inventory that you purchased for $10 each, so your total base-year inventory cost is $1,000.

Dollar-value LIFO is an accounting method utilized for inventory that follows the last-in-first-out model. Dollar-value LIFO involves this approach with all figures in dollar amounts, as opposed to in inventory units. It gives an alternate perspective on the balance sheet than other accounting methods, for example, first-in-first-out (FIFO). Remember, this is a simplified example and doesn’t take into account some of the complexities that can arise when you have multiple inventory pools or when prices decrease. Always consult with an accounting professional or financial advisor when dealing with inventory valuation. The LIFO retail inventory method employs the Last-in, First-out costing method to estimate ending inventory costs.

To solve delayering problem, we use traditional LIFO’s modified approach called Dollar-Value LIFO. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network.

This method may only suit specific industries where inventory quantity and value changes aren’t closely correlated. Additionally, companies should avoid creating unnecessary inventory pools to prevent increased complexity and costs. By using the latest prices first, cost of goods sold — or COGS — under LIFO is higher, and taxable income is lower, when compared to FIFO.

Under Dollar-Value LIFO, COGS tends to be higher because it reflects the most recent, and typically higher, costs of inventory. This increase in COGS reduces the gross profit margin, which in turn affects the net income. While this might seem disadvantageous at first glance, it can be beneficial from a tax perspective. Higher COGS leads to lower taxable income, thereby reducing the company’s tax liability.